The roll-up wave is hitting MRO distribution — and the consolidation playbook is entirely…. predictable.

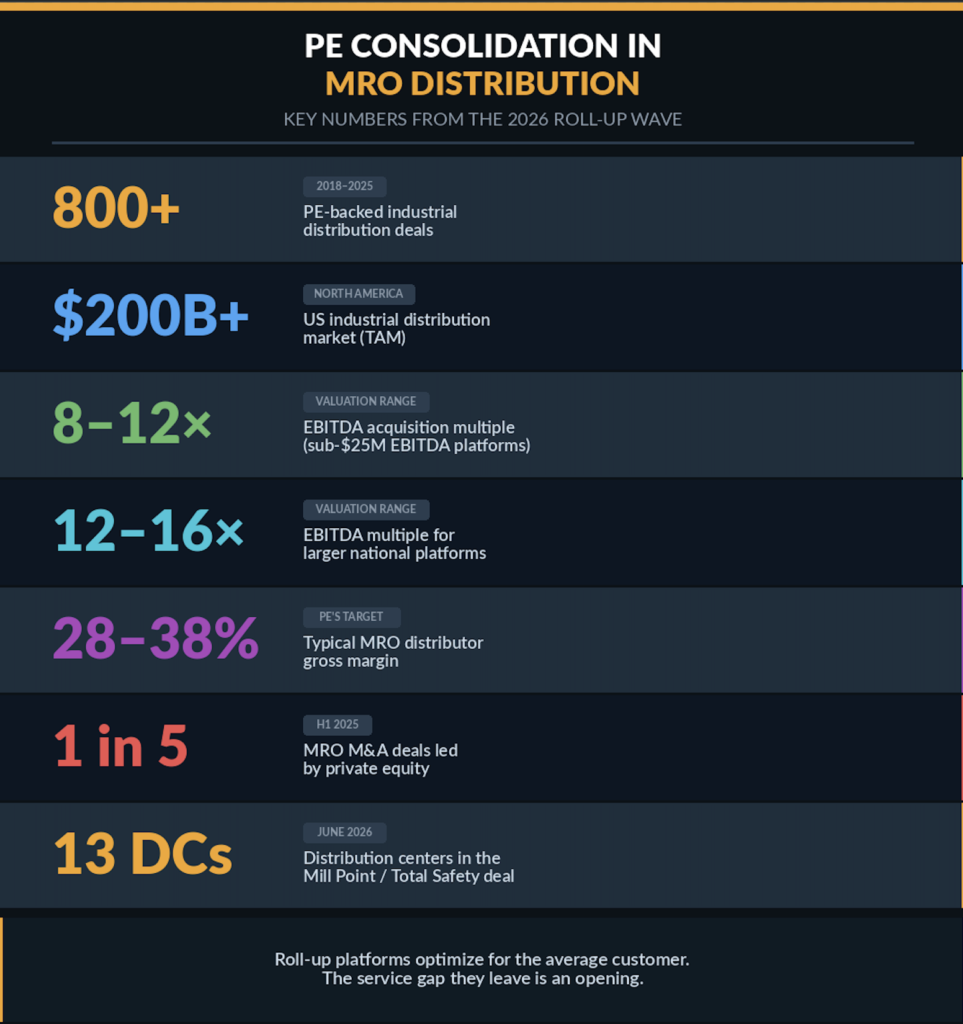

Since 2018, there have been more than 800 disclosed PE-backed industrial distribution transactions across North America.

The latest: NY Based Mill Point Capital just acquired the MRO distribution arm of Total Safety — 13 distribution centers, 20 onsite customer stores, and hundreds of vending machines servicing industrial facilities coast to coast.

This example is not a one-off deal. It’s the continuation of the most active consolidation cycle industrial distribution has seen to date.

US industrial distribution is a $200 billion-plus market — fragmented, relationship-driven, built on local trust and tribal knowledge. PE is now foaming at the mouth.

Private equity doesn’t buy businesses to run them the same way. It buys them to optimize them — which is a polite word for what happens to your service agreement next year.

That’s the real story.

Simple equations: at acquisition multiples of 8–16x EBITDA, new ownership needs somewhere to find the returns. Gross margins in MRO distribution typically run 28–38% and net margin is around 5.5%. That’s the target.

Here’s what the playbook looks like after the wire transfer clears:

None of this is speculation. It’s the standard 100-day integration plan, and it plays out the same way at every roll-up platform.

The only variable is how long it takes you to notice.

MDM’s 2026 Top Distributors list just dropped — and the headline writes itself: the biggest are getting bigger, fast.

That’s not going to slow down. The capital is there, the fragmentation is there, and PE has 800 data points proving the model works.

Here’s what that creates: a widening service gap.

Roll-up platforms are built to serve the average customer efficiently. Facilities with unusual SKU requirements, complex cross-references, tight lead time windows, or high-touch sourcing needs cost more than the new margin structure can absorb.

There is your opening.

The plant directors and procurement managers who see this cycle coming — who diversify their supply base before the integration ends — are the ones who don’t have a critical maintenance event turn into a production shutdown because a newly acquired distributor cut their SKU from the catalog.

The consolidators are going to keep buying. That’s fine, that’s good. The operators who pay attention are going to use the disruption to build a supply chain that doesn’t depend on whoever the current owner happens to be.

What to watch: distributor M&A activity in the back half of 2026 — the next wave is already in diligence.

Our team can locate, cross-reference, and source all parts.